Real estate investing is often synonymous with homeownership, as it is the most common form of real estate investment for individuals. However, real estate extends beyond personal residences and holds its own place as a distinct asset class within a diversified investment portfolio. Over the past five decades, it has gained significant popularity as an investment avenue.

When pursuing real estate investment opportunities, investors often encounter situations where they require immediate access to capital. This is where a residential hard money loan can come into play.

When typical financing sources are unavailable or not practical owing to credit concerns, unorthodox projects, or time-sensitive opportunities, real estate investors may choose to explore residential hard money loans. In comparison to conventional mortgages, these loans provide more flexibility in terms of qualifying requirements and a faster approval process.

How a Residential Hard Money Loan Works

A hard money loan, also known as bridge loan, is a temporary financing option utilized by real estate investors to fund investment projects. This loan is frequently used by real estate investors who require immediate funding for property acquisitions, repairs, or other investment ventures.

Unlike traditional banks, a residential hard money loan is provided by private lenders and is secured by the property itself. Standard bank loans mainly rely on creditworthiness and income verification while residential hard money lenders prioritize the value of the property and the borrower’s equity.

Best Uses of Hard Money Loans for Residential Properties

Hard money residential loans are primarily used by real estate investors for various purposes. This includes the following:

Flipping a House

Fix and flip ventures are popular among real estate investors specializing in purchasing troubled buildings, restoring or rehabilitating them, and selling them for a profit. Having a rapid turnaround time is critical in flipping. House flippers strive to finish repairs quickly in order to return the home to the market and sell it at a better price, ideally within a few months.

Hard money loans for residential properties, such as fix and flip loans, provide a valuable financing option for house flippers engaged in these ventures, by enabling them to swiftly acquire and improve distressed properties, thereby maximizing their potential for profit.

Buying an Investment Property

Investment property purchase is a fundamental use of hard money loans or bridge loans. As the name implies, it serves as a temporary financing solution that “bridges” the gap between the acquisition of a property and the securing of long-term financing or the completion of a specific event. They offer quick access to funds, allowing borrowers to take advantage of investment opportunities without delay.

Pros and Cons of a Residential Hard Money Loan

Although hard money loans offer certain advantages compared to traditional financing options, it is essential to be aware of their potential drawbacks. In order to provide a comprehensive understanding of this type of loan, we will explore both the benefits and disadvantages associated with hard money loans.

Advantages of a Residential Hard Money Loan

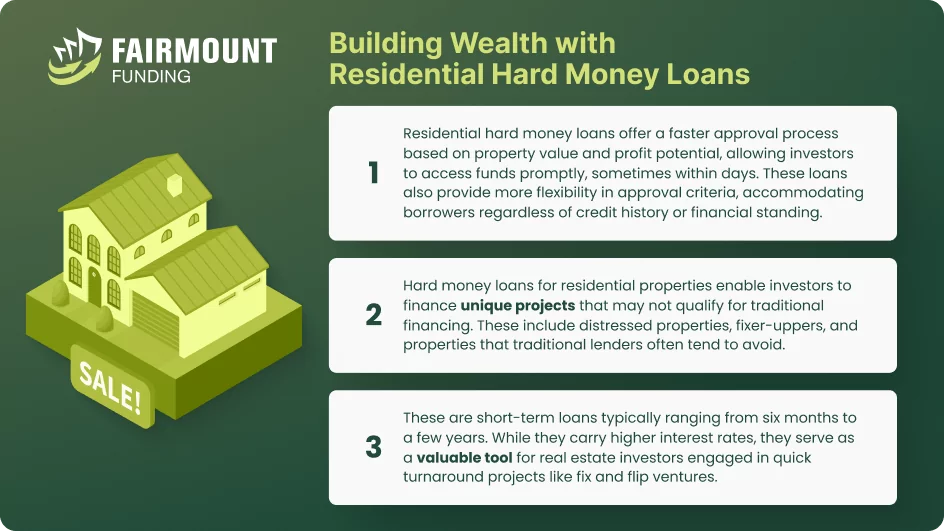

- Faster Approval and Funding. Hard money residential loans are typically evaluated based on the value of the property and the potential for profit. This allows for a quicker decision-making process, enabling borrowers to access funds promptly, sometimes within a matter of days.

- Flexible Approval Criteria. Hard money lenders for residential homes provide loans for borrowers, regardless of their credit history or financial standing. Borrowers have a better probability of acceptance if the property has enough value and potential as compared to traditional lenders who have stricter criteria. Furthermore, they offer more flexibility in terms of repayment structures.

- Ability to Finance Unique Properties. Properties that may not qualify for traditional financing due to their unique characteristics or condition can be financed by hard money residential loans. This includes distressed properties, fixer-uppers, and unconventional properties that may not meet the stringent requirements of traditional lenders.

Disadvantages of a Residential Hard Money Loan

- Higher Interest Rates and Fees. Because these loans are more risky for the residential hard money lenders, they charge higher interest rates to compensate. Borrowers may also face increased fees, such as origination fees, loan servicing fees, and prepayment penalties.

- Shorter Loan Terms. A residential hard money loan is a short term loan that typically ranges from six months to a few years. This short repayment period can put some borrowers under strain because they must return the loan soon or find alternative long-term financing solutions. This also results in higher monthly payments.

- Asset-Based Collateral. Borrowers are at risk of losing the property if they are unable to fulfill the repayment obligations since a residential hard money loan is primarily secured by the property itself.

Working with Residential Hard Money Lenders

When selecting a residential hard money lender, it is important to prioritize finding one aligned with your objectives. Given the large financial commitment involved in real estate finance, choosing one that has demonstrated success should be a primary consideration. While hard money lenders typically provide loans for a wide range of property types, certain investments are particularly suited for hard money financing.

Hard money works well with projects like rehab loans, construction loans, and land loans. These are often properties with a high potential for quick turnover and attractive selling prospects. Lenders are more likely to give financing for properties that are predicted to sell quickly and have a high selling potential.

As a borrower, you must concisely explain you intend to buy with the residential hard money loan and how much the expected value of it is. This includes what you’re planning, how much the cost is, the amount of your own capital you are investing, the projected timeline, and the anticipated value of the completed project. Thorough organization and attention to detail can significantly increase your chances of obtaining approval for a residential hard money loan.

While hard money loans typically carry higher interest rates compared to traditional mortgages, this factor may not be a significant concern for house flippers and short-term investors. Their strategy involves repaying the loan in the soonest time possible, minimizing the impact of the high interest rate and ultimately reducing the overall cost of the loan. Remember, the key advantage of a residential hard money loan is the speed. So, if you can wait for a few months for a loan approval, it might be better to check other options for you.

Residential Hard Money Loan FAQs

When is it appropriate to apply for a residential hard money loan?

A residential hard money loan is suitable in scenarios where traditional financing options may not be feasible or timely. This could include time-sensitive purchases, having less than perfect credit or limited credit history, property renovations or rehabilitations, bridge financing, and borrowers who may not have all the necessary documentation required by traditional lenders.

What are the risks associated with residential hard money loans?

Higher interest rates and fees, short-term repayment obligations, the possibility of property seizure in the event of default, limited regulatory protections, vulnerability to property value fluctuations, cash flow strain, and specific borrower qualifications are all inherent risks of residential hard money loans. Borrowers must carefully analyze these risks and do extensive due diligence before continuing with a residential hard money loan.

What qualifications do hard money residential lenders look for in a borrower?

Residential hard money lenders typically consider qualifications such as the property’s value, a clear exit strategy, financial capacity to make loan payments, and experience in real estate.

Requirements may vary among lenders, so it’s important for borrowers to research and communicate with potential lenders to understand their specific qualifications.

Understanding Hard Money Lenders

When compared to regular bank lending, working with hard money lenders is a unique experience. Hard money lenders, unlike regulated financial institutions, operate with greater flexibility and less restriction. This enables direct loan conditions and negotiations with lenders. Hard money lenders have discretion in determining eligibility criteria, including credit scores, debt-to-income ratios, and other factors. It is important to note that hard money lenders prioritize the potential return on investment when evaluating loan applications, making it a key consideration for borrowers.

KEY TAKEAWAYS

- The primary benefit of a residential hard money loan lies in its ability to provide speedy financing.

- Residential hard money lenders have considerable autonomy when it comes to establishing their own criteria that borrowers must meet.

- Borrowers have the opportunity to negotiate and customize the loan terms to best suit their individual requirements.